Key Points

- While there is a need for regulations on the charitable sector to foster accountability and trust in charities, excessive levels of regulation impose a burden on charities that outweighs the benefit of the regulation.

- Little research has been done to examine the impact of overregulation on the charitable sector. This study is a first step toward gaining a better understanding of the regulatory burden imposed on charities.

- By comparing states along five categories of charitable regulations, one can see that overregulation is correlated with relatively fewer charities in a state.

- Our society and those in need depend on a thriving, vibrant charitable sector. The evidence in this study suggests excessive levels of regulation are counterproductive to fostering a positive environment for charities and those they serve.

Executive Summary

Ideally, state regulations on charitable organizations impose minimal costs relative to their benefits in terms of creating improved transparency and accountability. Like any other good or service, the benefits provided by regulation exhibit diminishing returns indicating that as the number of mandates increases, and the complexity of the regulatory structure grows, the additional benefits enabled by the regulations decline.

While the benefits gained from imposing additional regulations decline, the costs associated with complying with these mandates will increase. More burdensome state regulatory structures require charities to devote larger amounts of personnel time, money and other resources toward complying with the state mandates rather than fulfilling their charitable missions. The net value enabled by regulations will tend to decrease, consequently, as the size and complexity of their burdens grow. Further, a growing regulatory burden expands the divide between the value of the resources dedicated toward charitable efforts and the amount of public benefit these organizations can provide.

Therefore, states that impose an excessive regulatory burden undermine the efficiency and effectiveness of the charitable sector.1

The way states regulate charitable organizations varies significantly, indicating the relative burdens from state regulations differ. While understanding how these burdens vary can help states create a more efficient regulatory environment, there are few resources available that provide a comprehensive comparison of the impact state regulations have on charitable organizations. The purpose of this study is to provide a broad review of state regulations to help begin to fill this gap.

The analysis classifies state regulations of charities into five categories comprised of measures that reflect the diverse types of regulations implemented by at least one state. The categories include: start-up regulations, annual reporting requirements, rules for paid solicitors, audit mandates and oversight regulations.

These categories are included because they comprise the main features of the charitable regulatory landscape. This analysis does not argue that any one specific type of regulation discussed here should be eliminated. Rather, that the full compliance burdens on charities should be weighed against the benefit of the regulations.

These five categories were weighted equally, and states were ranked separately based on the measures for each category. The state with the lowest score is ranked as having the “least burdensome regulatory environment” and receives the top rank, while the state with the highest score receives the lowest rank.2 Summing the ranks across the five regulatory categories provides the basis for the overall state rankings. The overall state rankings of the top five (or best) and bottom five (or worst) states are below.

The five states with the friendliest regulatory environment toward charitable organizations are Montana, Wyoming, Nebraska, Delaware and Idaho. The five states with the most burdensome regulatory environment toward charitable organizations are Connecticut, Mississippi, New Jersey, Florida and Pennsylvania. Relating these rankings to the vibrancy of the charitable sector (as measured by the number of charities per billion dollars of GDP) provides initial perspective regarding the consequences from imposing a more burdensome regulatory environment on charitable organizations. There is, in fact, a strong correlation between the states that impose more burdensome regulatory environments and the vibrancy of the charitable sector. While more research is required, the results are an initial indication that the states imposing the most burdensome regulatory environments are dimming the vibrancy of the charitable sector. Consequently, states should consider the benefits from streamlining state regulations and eliminating unnecessary burdens as a means for promoting a more efficient and effective charitable sector.

Best and Worst

Top States by Charitable Regulatory Burden

| Top Five (Lightest Burden) | Overall Ranking |

|---|---|

| Montana | 1 |

| Wyoming | 2 |

| Nebraska | 3 |

| Delaware | 4 |

| Idaho | 5 |

Bottom States by Charitable Regulatory Burden

| Bottom Five (Heaviest Burden) | Overall Ranking |

|---|---|

| Connecticut | 46 |

| Mississippi | 47 |

| New Jersey | 48 |

| Florida | 49 |

| Pennsylvania | 50 |

Introduction

How states regulate businesses and nonprofits matters. Some states enact costly regulatory mandates that impose large financial compliance burdens on organizations. Others take a less burdensome approach. Making matters more complicated, often states enact onerous regulations on some activities but take a lighter regulatory approach in other areas.

It is well established that excessive regulatory burdens meaningfully impact business profitability and, consequently, economic outcomes. A 2020 Mercatus Center analysis of the costs from federal regulations found that:

Economic growth in the United States has, on average, been slowed by 0.8% per year since 1980 owing to the cumulative effects of regulation:

- If regulation had been held constant at levels observed in 1980, the U.S. economy would have been about 25% larger than it was as of 2012.

- This means that in 2012, the economy was $4 trillion smaller than it would have been in the absence of regulatory growth since 1980.

- This amounts to a loss of approximately $13,000 per capita, a significant amount of money for most American workers.3

Excessive regulations at the state level have deleterious impacts as well. California, for instance, imposes an overly burdensome regulatory environment on for-profit organizations. Chambers and O’Reilly found that, “The increase in California’s regulatory burden from 1997 to 2015 is associated with an increase in the number of people living in poverty by 512,906 individuals (4,972,955 after vs. 4,460,049 before) and an increase in the poverty rate of 1.32 percentage points (12.8% after vs. 11.48% before).”4 Due to their large economic consequences, there are many studies assessing how state regulatory environments impact for-profit organizations and overall economic performance, including the Pacific Research Institute’s “50-State Small Business Regulation Index.”5

However, state regulations also impact the financial costs and the amount of personnel time that must be devoted toward regulatory compliance by charities.6 To the extent that state regulations impose minimal costs and improve transparency and accountability, there are benefits from these mandates.

The impact from regulations becomes a net negative when, as with the for-profit sector, they grow to excessive levels. When regulations become overly burdensome, charitable organizations must devote excessive amounts of staff time, money and other resources toward complying with the regulatory state rather than fulfilling their missions.7

Just like with for-profit organizations, the way states regulate charitable organizations varies significantly. Unlike with businesses, there are significantly fewer resources available that provide a comprehensive comparison of how state regulations impact charitable organizations.8 This study aims to help fill this need by ranking the 50 states based on each state’s relative regulatory burden on charities.

Methodology: Ranking the States

To rank the states, the analysis classifies state regulations of charities into five categories. Each category is comprised of measures that reflect the diverse types of regulations that at least one state implements. Federal regulations will impact charities regardless of their state location and are, consequently, not considered.

Each regulatory measure falls into one of two types. The first type simply documents whether a state imposes the identified regulation; for instance, are purchases by charitable organizations exempt from the state sales taxes or not. For quantifying the impact, those states that do not impose the deleterious regulation under consideration are given a rank of one for the measure (the top rank). Those states that promulgate the burdensome regulation are given a rank of 50 (the worst rank). In certain categories, some states impose a less burdensome form of the regulations and receive an intermediary ranking (e.g., 25).

The second type of measure quantifies the varied burdens created by the state regulation in question; for instance, the dollar cost charged by the state for filing the required annual government forms. State regulations that impose the lowest cost receive a rank of one. The states that charge higher fees and, consequently, impose a higher burden receive sequentially higher ranks, with the state with the relatively costliest regulation receiving a rank of 50.

Each category is comprised of measures that reflect the diverse types of regulations that at least one state implements.

When regulations become overly burdensome, charitable organizations must devote excessive amounts of staff time, money and other resources toward complying with the regulatory state rather than fulfilling their missions.

THE FIVE REGULATORY CATEGORIES EXAMINED (ALONG WITH THE SPECIFIC REGULATORY MEASURES FOR EACH CATEGORY) ARE LISTED BELOW.

- Start-up regulations, or the regulatory burdens associated with starting a new charity. This category ranks each state based on whether the state requires registration by charitable organizations; the top registration fee charged; the top incorporation fee(s) charged and whether charitable organizations must also apply for the state corporate income tax exemption after receiving their federal exemption.

- Annual reporting and filing regulations, or the annual regulatory burdens organizations must comply with. This category ranks each state based on the dollar value of the annual fees the state charges, whether charities must file an annual report, whether charities must file any additional annual filings and the size of any additional annual filing fees.

- Paid solicitor regulations, or the regulatory burdens imposed on the use of paid solicitors to help charities raise money. This category ranks each state based on the dollar value of the paid solicitor registration fee, paid solicitor renewal fees, whether surety bonds for professional fundraisers are required, whether fundraisers are required to provide notice before a solicitation campaign, whether registration by fundraising counsel are required, whether commercial fundraisers must register with the state, whether annual financial reporting by commercial fundraisers is required and whether charities must file copies of the contracts between charitable organizations and commercial fundraisers.

- Audit requirements, or the stringency of the state’s audit mandates. This category ranks each state based on whether an independent audit by a certified public accountant (CPA) is required and, for those states that require an independent CPA audit, whether a revenue threshold for an audit requirement exists and whether a revenue threshold for an annual review (a lesser burden than a full audit) exists. The rankings also account for whether those states that do not require an independent CPA audit do require an audit for public contracts.

- Oversight regulations, or the general regulatory environment for charities and nonprofits, includes issues such as whether the state is a bifurcated jurisdiction or an attorney general-only regulated jurisdiction, whether charities are exempt from state sales and use taxes, the oversight requirements for any potential commercial co-ventures for a charity and whether charitable contributions are tax deductible for residents.

TABLE 1

50-STATE RANKINGS OF CHARITY REGULATIONS

| State | Total Rank by Category |

|---|---|

| Montana | 1 |

| Wyoming | 2 |

| Nebraska | 3 |

| Delaware | 4 |

| Idaho | 5 |

| Iowa | 6 |

| South Dakota | 7 |

| Arizona | 8 |

| Nevada | 9 |

| Texas | 10 |

| Vermont | 11 |

| Kentucky | 12 |

| North Dakota | 13 |

| Missouri | 14 |

| Oklahoma | 15 |

| New Mexico | 16 |

| Colorado | 17 |

| Indiana | 18 |

| Oregon | 19 |

| Alabama | 20 |

| Alaska | 21 |

| Utah | 22 |

| Michigan | 23 |

| Louisiana | 24 |

| South Carolina | 25 |

| Ohio | 26 |

| Washington | 27 |

| Illinois | 28 |

| Arkansas | 29 |

| Wisconsin | 30 |

| New York | 31 |

| Maine | 32 |

| Minnesota | 33 |

| North Carolina | 34 |

| Kansas | 35 |

| New Hampshire | 36 |

| West Virginia | 37 |

| Virginia | 38 |

| Rhode Island | 39 |

| Georgia | 40 |

| Tennessee | 41 |

| California | 42 |

| Hawaii | 43 |

| Massachusetts | 44 |

| Maryland | 45 |

| Connecticut | 46 |

| Mississippi | 47 |

| New Jersey | 48 |

| Florida | 49 |

| Pennsylvania | 50 |

To ensure equal weighting across the five categories for the final ranking, the score for each regulatory category is the average ranking across all the measures that comprise the category. The state with the lowest average score is ranked as having the “least burdensome regulatory environment” for that category. Summing the ranks across the five regulatory categories provides the basis for the overall state rankings, which are presented in Table 1. The state with the lowest number receives the top rank, while the state with the highest value receives the worst rank.9

The five states with the friendliest regulatory environment toward charitable organizations are Montana, Wyoming, Nebraska, Delaware and Idaho. The five states with the most burdensome regulatory environment toward charitable organizations are Connecticut, Mississippi, New Jersey, Florida and Pennsylvania.

It is important to note that this is an imperfect ranking based on imperfect variables. As examined later in this report, there are regulatory burdens in some of the “top” states that may be onerous relative to the cost imposed on charities. Likewise, there are regulations in some of the “bottom” states that reflect effective, balanced approaches to regulating the sector. There may also be complex exemptions to certain regulations that are not possible to capture in this analysis. Further, there are differing approaches to how these regulations are set by state. Some of what is discussed in this report is found in state statute as enacted by legislative bodies. Other rules are administrative regulations implemented by executive bodies charged with oversight of the state’s charities. The methodology and findings of this report point to the need for more research on this topic. However, despite these limitations, the ranking offers one approach to compare regulatory burden across state lines.

More Regulations, Fewer Charities

Comparing the charitable organization data maintained by the IRS to the state charity regulatory rankings in Table 1 suggests that the states imposing more burdensome regulatory environments are dimming the vibrancy of their charitable sectors.

Specifically, the IRS maintains data on the total number of charitable organizations that qualify for tax deductions in every state.10 These data need to be adjusted, however, because populations and economic output vary greatly between the states and these factors, as well as others not considered here, will impact the total number of charities that are incorporated. There is no perfect way to adjust these data, but as a first step toward gaining insight on the impact of overregulation on the health of a state’s charitable sector, there are reasonable assumptions that can be made.

For the purposes of this analysis, we assume there is a positive relationship between the number of people living in a state, as well as the state’s economic output, and the number of charitable organizations operating in the state, regardless of its regulatory environments. Adjustments that account for these differences are useful before comparing the state rankings to the number of charitable organizations.

While there are myriad ways the data could be adjusted, this analysis uses state gross domestic product (GDP) to adjust for state size rather than population because there is also a strong relationship between economic growth and charitable giving. As Rooney and Bergdoll (2020) noted:

“There’s a strong relationship between how much money Americans give to charity and their aftertax income. There is a similar correlation between giving and the stock market’s performance. That means people give more when they feel that they have money to spare.”11

Consequently, to account for the varied size of each state and each state’s economy, the analysis compares each state’s charity ranking to the total number of charities per billion dollars of state GDP.

Consistent with the hypothesis that there will be fewer charities in states that impose more burdensome regulatory environments, the overall state rankings are negatively correlated with the number of charities per billion dollars of state GDP. The states with a less burdensome regulatory environment (a lower ranking number) tend to have more charitable organizations per billion dollars of GDP.12 More research is required to determine if there is a causal relationship as well as a clear correlation.

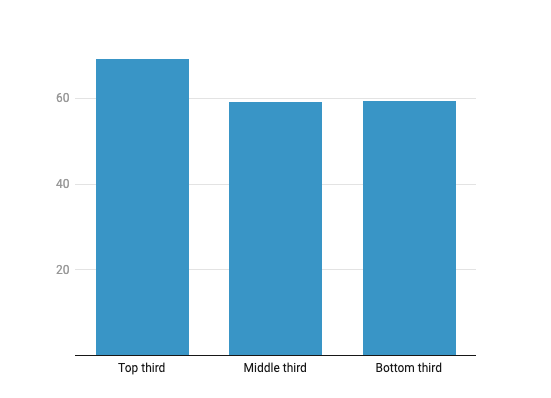

To visualize this relationship, Figure 1 presents the average number of charities per billion dollars of GDP in the states ranked in the top third, middle third and bottom third. Figure 1 clearly shows more charitable organizations exist in the states that impose the least burdensome regulatory environments.

Specifically, the states in the top one-third of the regulatory rankings have, on average, 68.03 charities per $1 billion in GDP, which is significantly higher than the average number of charities per $1 billion in GDP for the middle third (15.5% higher) and bottom third (14.8% higher) of the rankings.

FIGURE 1

NUMBER OF CHARITABLE ORGANIZATIONS PER $1 BILLION IN GDP BY REGULATORY RANKING

Implications

Overall, these results indicate that the states in the bottom two-thirds of the rankings may be able to increase the amount of charitable activity in their states by replicating the regulatory environment of the states in the top-third of the rankings. The bottom-ranked states scored poorly across most of the categories, as demonstrated in Table 2. Table 2 presents the rankings for each of the five categories and the overall rank for the five worst performing states.

TABLE 2

CATEGORY RANKINGS FOR FIVE LOWEST RANKED STATES

| State | Start-Up Regulations | Annual Reporting / Filing | Paid Solicitor Fees and Regulations | Audit Requirements | Oversight Regulations | Total Rank by Category |

|---|---|---|---|---|---|---|

| Connecticut | 38 | 39 | 28 | 36 | 50 | 46 |

| Mississippi | 38 | 16 | 47 | 49 | 50 | 47 |

| New Jersey | 47 | 38 | 28 | 36 | 50 | 48 |

| Florida | 44 | 46 | 46 | 31 | 50 | 49 |

| Pennsylvania | 49 | 43 | 32 | 44 | 50 | 50 |

The category rankings in these five states were consistently in the bottom half for all the categories, often in the bottom 10 states. Consistent with their poor rankings, the average number of charities per billion dollars of GDP in the five worst performing states was 58.64, which is 1.1% less than the average for the bottom third of the states. The consistently poor performance across all the categories indicates that improving the regulatory environment in the lowest-ranked states requires a broad array of reforms, which could improve the amount of charitable activity in these states.

At the other end of the rankings, the five states that impose the least burdensome regulatory environment generally promulgate relatively lower regulatory burdens across all the categories – albeit each state had room for improvement in at least one category, see Table 3. And, consistent with the pattern, the average number of charities in the top performing states per billion dollars of GDP was 75.94, or 11.6% more than the average for the states in the top third of the rankings.

TABLE 3

CATEGORY RANKINGS FOR FIVE HIGHEST RANKED STATES

| State | Start-Up Regulations | Annual Reporting / Filing | Paid Solicitor Fees and Regulations | Audit Requirements | Oversight Regulations | Total Rank by Category |

|---|---|---|---|---|---|---|

| Montana | 3 | 8 | 1 | 1 | 1 | 1 |

| Wyoming | 5 | 9 | 1 | 1 | 1 | 2 |

| Nebraska | 2 | 2 | 1 | 1 | 17 | 3 |

| Delaware | 8 | 9 | 1 | 1 | 1 | 4 |

| Idaho | 11 | 3 | 1 | 1 | 17 | 5 |

While these results have important implications, it is imperative to note that significantly more research into the impact of regulations on charitable organizations is necessary to enhance our understanding of these important issues. The rankings developed here provide a first step toward this goal.

Overall, these results indicate that the states in the bottom twothirds of the rankings may be able to increase the amount of charitable activity in their states by replicating the regulatory environment of the states in the top-third of the rankings.

Developing the Rankings

Having summarized the findings, the remainder of this paper provides greater detail on the sources and methods used to create the rankings and is organized by the five regulatory categories that comprise the overall rankings. The rankings leveraged several key data resources to establish these ordinal rankings.13 The following series of tables present the state rankings for each measure and category, with the underlying data presented in the Data Appendices.

CATEGORY 1:

START-UP REGULATIONS

The start-up regulations category compares the burdens states impose to start a charitable organization based on four measures. The first measure is registration requirements, which 40 states impose.14 Often, the state registration requirements are duplicative to federal requirements while providing little useful information to the state authorities. Further, state authorities rarely act on this information.15 Consequently, registration requirements too often add additional compliance burdens on new charitable organizations without necessarily creating any offsetting benefits.

Similarly, expensive registration and incorporation fees, while perhaps trivial costs for well-funded start-up charities, can impose significant obstacles for start-ups that are lacking financial resources. To account for these start-up obstacles, Table 4 presents the state rankings for top registration fee and incorporation fee. Finally, the ability for income to be tax exempt from state income taxation (in those states that levy a corporate income tax) is an important benefit for nonprofits. Some states require an additional application to receive the state corporate income tax exemption once the federal tax exemption has been received, however. This filing creates additional burdens in those states.

TABLE 4

START-UP REGULATION RANKING

| State | Start-Up Regulations Ranking | Top Registration Fee | Incorporation Fees | Requires Registration by Charitable Organizations | Must Apply for Exemption from State Corporate Income Tax |

|---|---|---|---|---|---|

| Alabama | 23 | 22 | 44 | 50 | 1 |

| Alaska | 36 | 31 | 28 | 50 | 50 |

| Arizona | 7 | 1 | 25 | 1 | 1 |

| Arkansas | 26 | 1 | 28 | 50 | 50 |

| California | 33 | 22 | 28 | 50 | 50 |

| Colorado | 15 | 18 | 28 | 50 | 1 |

| Connecticut | 38 | 32 | 28 | 50 | 50 |

| Delaware | 8 | 1 | 43 | 1 | 1 |

| Florida | 44 | 50 | 21 | 50 | 50 |

| Georgia | 45 | 29 | 44 | 50 | 50 |

| Hawaii | 22 | 1 | 8 | 50 | 50 |

| Idaho | 11 | 1 | 17 | 1 | 50 |

| Illinois | 16 | 19 | 28 | 50 | 1 |

| Indiana | 1 | 1 | 1 | 1 | 1 |

| Iowa | 3 | 1 | 4 | 1 | 1 |

| Kansas | 29 | 29 | 4 | 50 | 50 |

| Kentucky | 18 | 1 | 2 | 50 | 50 |

| Louisiana | 38 | 22 | 38 | 50 | 50 |

| Maine | 34 | 32 | 25 | 50 | 50 |

| Maryland | 50 | 49 | 47 | 50 | 50 |

| Massachusetts | 43 | 41 | 21 | 50 | 50 |

| Michigan | 19 | 1 | 4 | 50 | 50 |

| Minnesota | 36 | 22 | 37 | 50 | 50 |

| Mississippi | 38 | 32 | 28 | 50 | 50 |

| Missouri | 24 | 19 | 8 | 50 | 50 |

| Montana | 3 | 1 | 4 | 1 | 1 |

| Nebraska | 2 | 1 | 3 | 1 | 1 |

| Nevada | 13 | 1 | 38 | 50 | 1 |

| New Hampshire | 27 | 22 | 8 | 50 | 50 |

| New Jersey | 47 | 46 | 38 | 50 | 50 |

| New Mexico | 10 | 1 | 8 | 50 | 1 |

| New York | 38 | 22 | 38 | 50 | 50 |

| North Carolina | 46 | 44 | 36 | 50 | 50 |

| North Dakota | 16 | 22 | 25 | 50 | 1 |

| Ohio | 48 | 44 | 48 | 50 | 50 |

| Oklahoma | 32 | 39 | 8 | 50 | 50 |

| Oregon | 12 | 1 | 28 | 50 | 1 |

| Pennsylvania | 49 | 46 | 48 | 50 | 50 |

| Rhode Island | 42 | 40 | 21 | 50 | 50 |

| South Carolina | 30 | 32 | 8 | 50 | 50 |

| South Dakota | 6 | 1 | 17 | 1 | 1 |

| Tennessee | 24 | 32 | 44 | 50 | 1 |

| Texas | 19 | 46 | 8 | 50 | 1 |

| Utah | 35 | 41 | 17 | 50 | 50 |

| Vermont | 9 | 1 | 48 | 1 | 1 |

| Virginia | 27 | 41 | 38 | 50 | 1 |

| Washington | 21 | 38 | 17 | 50 | 1 |

| West Virginia | 30 | 32 | 8 | 50 | 50 |

| Wisconsin | 14 | 19 | 21 | 50 | 1 |

| Wyoming | 5 | 1 | 8 | 1 | 1 |

Equally weighting the categories, Indiana, Nebraska, Iowa, Montana and Wyoming impose the least burdensome start-up environment for nonprofits and charities. Maryland, Pennsylvania, Ohio, New Jersey and North Carolina impose the most burdensome start-up environment.

CATEGORY 2:

ANNUAL REPORTING AND FILING REGULATIONS

Charities and nonprofits must also comply with annual regulatory burdens that vary significantly across the states. For starters, the annual filing fees vary from no annual fee (in Arkansas, Colorado, Idaho, Iowa, New Mexico, Pennsylvania, Texas and Vermont) to a high of $1,525 in New York. The annual filing fee is not the only potential annual cost either. Many states impose additional annual fees that charities must also pay that can be as high as $2,000, which is the maximum fee charities must pay in order to file required annual forms in Massachusetts, depending upon the organization’s revenues. These additional annual fees increase the cost of operations for charities making it more difficult for these organizations to fulfill their missions.

Along with the annual fees, states also require charities to file reports with the state on regular intervals.16 These reports include an annual report, which is required in 47 states – Alaska requires a biennial filing. In addition to an annual report, many states also require supplemental report filings that include annual financial reports, annual solicitation reports and registration renewals.

TABLE 5

ANNUAL REPORTING AND FILING REGULATIONS AND RANKING

| State | Annual Reporting Regulations Ranking | Highest Annual Fee | Highest Additional Annual Filing Fees | Annual Report Filing Requirements | Additional Annual Filing Requirements |

|---|---|---|---|---|---|

| Alabama | 9 | 26 | 1 | 50 | 1 |

| Alaska | 24 | 35 | 32 | 25 | 17 |

| Arizona | 12 | 11 | 1 | 50 | 17 |

| Arkansas | 7 | 1 | 1 | 50 | 17 |

| California | 50 | 48 | 38 | 50 | 50 |

| Colorado | 28 | 1 | 30 | 50 | 33 |

| Connecticut | 39 | 37 | 39 | 50 | 17 |

| Delaware | 9 | 26 | 1 | 50 | 1 |

| Florida | 46 | 41 | 48 | 50 | 17 |

| Georgia | 42 | 33 | 30 | 50 | 33 |

| Hawaii | 47 | 9 | 49 | 50 | 50 |

| Idaho | 3 | 1 | 1 | 50 | 1 |

| Illinois | 22 | 11 | 28 | 50 | 17 |

| Indiana | 12 | 11 | 1 | 50 | 17 |

| Iowa | 1 | 1 | 1 | 25 | 1 |

| Kansas | 37 | 35 | 35 | 50 | 17 |

| Kentucky | 15 | 18 | 1 | 50 | 17 |

| Louisiana | 4 | 9 | 1 | 50 | 1 |

| Maine | 33 | 34 | 32 | 50 | 17 |

| Maryland | 41 | 44 | 1 | 50 | 50 |

| Massachusetts | 35 | 18 | 50 | 50 | 17 |

| Michigan | 17 | 22 | 1 | 50 | 17 |

| Minnesota | 31 | 26 | 35 | 50 | 17 |

| Mississippi | 16 | 37 | 1 | 50 | 1 |

| Missouri | 27 | 18 | 28 | 50 | 17 |

| Montana | 8 | 18 | 1 | 50 | 1 |

| Nebraska | 2 | 22 | 1 | 25 | 1 |

| Nevada | 18 | 26 | 1 | 50 | 17 |

| New Hampshire | 35 | 43 | 25 | 50 | 17 |

| New Jersey | 38 | 26 | 45 | 50 | 17 |

| New Mexico | 18 | 1 | 26 | 50 | 17 |

| New York | 21 | 50 | 1 | 50 | 1 |

| North Carolina | 26 | 44 | 1 | 50 | 17 |

| North Dakota | 5 | 11 | 1 | 50 | 1 |

| Ohio | 39 | 44 | 32 | 50 | 17 |

| Oklahoma | 25 | 42 | 1 | 50 | 17 |

| Oregon | 49 | 44 | 39 | 50 | 33 |

| Pennsylvania | 43 | 1 | 47 | 50 | 50 |

| Rhode Island | 48 | 22 | 43 | 50 | 50 |

| South Carolina | 30 | 37 | 1 | 50 | 33 |

| South Dakota | 5 | 11 | 1 | 50 | 1 |

| Tennessee | 45 | 22 | 44 | 50 | 33 |

| Texas | 14 | 1 | 46 | 1 | 33 |

| Utah | 29 | 11 | 42 | 50 | 17 |

| Vermont | 18 | 1 | 26 | 50 | 17 |

| Virginia | 33 | 49 | 1 | 50 | 33 |

| Washington | 32 | 11 | 37 | 50 | 33 |

| West Virginia | 43 | 26 | 39 | 50 | 33 |

| Wisconsin | 23 | 40 | 1 | 50 | 17 |

| Wyoming | 9 | 26 | 1 | 50 | 1 |

Table 5 demonstrates that Iowa, Nebraska, Idaho, Louisiana, North Dakota and South Dakota impose the smallest annual reporting burdens on charities, while Florida, Hawaii, Rhode Island, Oregon and California impose the most burdensome annual reporting requirements.

CATEGORY 3:

PAID SOLICITATION REGULATIONS

When the relationship is structured well, paid solicitors can be an important part of a charitable organization’s fundraising strategy. States take varied approaches to regulating paid solicitors that, when excessive, lead to higher costs for those charities that could benefit from these services. These costs include paid solicitor registration and renewal fees that can be as high as $1,000 in Indiana and Massachusetts. They also include surety bonds requirements that can be as high as $50,000 in Florida and North Carolina. Paid solicitors are also subjected to registration and notice requirements that include providing notice to the state before a solicitation campaign, registration requirements on fundraising counsels, registration requirements for commercial fundraisers, annual financial reporting requirements and requirements on charities to file copies of the contracts between charitable organizations and commercial fundraisers.

TABLE 6

PAID SOLICITOR REGULATIONS AND RANKING

| State | Paid Solicitor Rankings | Solicitor Renewal Fees | Paid Solicitor Registration Fee | Surety Bond for Professional Fundraisers | Notice before Solicitation Campaign | Registration by Commercial Fundraiser | Registration by Fundraising Counsel | Annual Financial Reporting by Commercial Fundraisers | Filing of Contracts between Charities and Commercial Fundraisers |

|---|---|---|---|---|---|---|---|---|---|

| Alabama | 25 | 1 | 19 | 1 | 50 | 1 | 50 | 50 | 50 |

| Alaska | 24 | 1 | 44 | 19 | 1 | 50 | 1 | 50 | 50 |

| Arizona | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| Arkansas | 35 | 1 | 1 | 1 | 50 | 50 | 1 | 50 | 50 |

| California | 43 | 1 | 1 | 37 | 50 | 50 | 1 | 50 | 50 |

| Colorado | 12 | 1 | 1 | 1 | 50 | 1 | 50 | 50 | 1 |

| Connecticut | 28 | 1 | 1 | 29 | 50 | 50 | 1 | 50 | 50 |

| Delaware | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| Florida | 46 | 1 | 1 | 50 | 50 | 50 | 1 | 50 | 50 |

| Georgia | 25 | 1 | 1 | 19 | 50 | 50 | 1 | 50 | 50 |

| Hawaii | 32 | 1 | 1 | 37 | 50 | 50 | 1 | 50 | 50 |

| Idaho | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| Illinois | 38 | 1 | 41 | 19 | 1 | 50 | 50 | 50 | 50 |

| Indiana | 50 | 50 | 50 | 1 | 50 | 50 | 50 | 50 | 50 |

| Iowa | 11 | 1 | 1 | 39 | 1 | 1 | 50 | 1 | 50 |

| Kansas | 22 | 1 | 1 | 1 | 1 | 50 | 50 | 50 | 50 |

| Kentucky | 42 | 1 | 48 | 37 | 1 | 50 | 50 | 50 | 50 |

| Louisiana | 17 | 1 | 42 | 37 | 1 | 50 | 1 | 50 | 50 |

| Maine | 19 | 1 | 46 | 37 | 1 | 1 | 50 | 1 | 50 |

| Maryland | 49 | 1 | 49 | 37 | 50 | 50 | 50 | 50 | 50 |

| Massachusetts | 43 | 1 | 50 | 37 | 1 | 50 | 50 | 50 | 50 |

| Michigan | 14 | 1 | 1 | 19 | 1 | 50 | 1 | 50 | 50 |

| Minnesota | 48 | 1 | 44 | 29 | 50 | 50 | 50 | 50 | 50 |

| Mississippi | 47 | 1 | 46 | 19 | 50 | 50 | 50 | 50 | 50 |

| Missouri | 21 | 50 | 40 | 1 | 1 | 50 | 1 | 50 | 1 |

| Montana | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| Nebraska | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| Nevada | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| New Hampshire | 39 | 1 | 42 | 29 | 50 | 50 | 50 | 50 | 50 |

| New Jersey | 28 | 1 | 1 | 29 | 1 | 50 | 50 | 50 | 50 |

| New Mexico | 9 | 1 | 1 | 37 | 1 | 50 | 1 | 50 | 50 |

| New York | 25 | 1 | 1 | 19 | 1 | 50 | 50 | 50 | 50 |

| North Carolina | 35 | 1 | 50 | 1 | 50 | 50 | 50 | 50 | 50 |

| North Dakota | 17 | 1 | 1 | 29 | 1 | 50 | 1 | 50 | 50 |

| Ohio | 32 | 1 | 1 | 37 | 50 | 50 | 1 | 50 | 50 |

| Oklahoma | 8 | 1 | 1 | 1 | 1 | 50 | 1 | 1 | 1 |

| Oregon | 35 | 1 | 1 | 1 | 50 | 50 | 50 | 50 | 50 |

| Pennsylvania | 32 | 1 | 1 | 37 | 1 | 50 | 50 | 50 | 50 |

| Rhode Island | 14 | 1 | 1 | 19 | 1 | 50 | 50 | 1 | 50 |

| South Carolina | 40 | 1 | 1 | 28 | 50 | 50 | 50 | 50 | 50 |

| South Dakota | 12 | 1 | 1 | 1 | 50 | 50 | 50 | 1 | 50 |

| Tennessee | 43 | 1 | 1 | 37 | 50 | 50 | 50 | 50 | 50 |

| Texas | 9 | 1 | 1 | 37 | 1 | 1 | 1 | 50 | 50 |

| Utah | 22 | 1 | 1 | 1 | 50 | 50 | 50 | 50 | 50 |

| Vermont | 28 | 1 | 1 | 29 | 50 | 50 | 50 | 1 | 50 |

| Virginia | 28 | 1 | 1 | 29 | 1 | 50 | 50 | 50 | 50 |

| Washington | 20 | 1 | 1 | 37 | 1 | 50 | 1 | 50 | 50 |

| West Virginia | 14 | 1 | 1 | 19 | 1 | 50 | 1 | 50 | 50 |

| Wisconsin | 41 | 1 | 1 | 29 | 50 | 50 | 50 | 50 | 50 |

| Wyoming | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

Table 6 demonstrates that Arizona, Delaware, Idaho, Montana, Nebraska, Nevada and Wyoming are all tied for imposing the smallest annual reporting burdens on paid solicitors, while Florida, Mississippi, Minnesota, Maryland and Indiana impose the most burdensome requirements on paid solicitors.

CATEGORY 4:

AUDIT REQUIREMENTS

The stringency of the state’s audit mandates is a key regulatory cost that many charities must bear.17 The primary question for this category is whether an independent CPA audit is required. Those states that do not require an independent CPA audit are Alabama, Arizona, Colorado, Delaware, Idaho, Indiana, Iowa, Kentucky, Louisiana, Missouri, Montana, Nebraska, Nevada, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, South Carolina, South Dakota, Texas, Utah, Vermont and Wyoming. These states are given a rank of 1 in Table 7 except Indiana, Louisiana and North Carolina, which require independent audits when a charity has a public contract. These states are ranked as having more expensive regulations than the states with no audit requirements but lower than the states that require independent audits broadly speaking.

For those states that do require independent audits, many impose revenue thresholds below which the charity is exempt from the audit requirements. The remaining states are consequently ranked based on how high the threshold is – the higher the threshold, the lower the state’s ranking because more charities are exempted from the burden of a comprehensive audit. Several of these states also create an additional revenue threshold, which establishes a lower benchmark for charities. The charities with revenues between the lower and upper thresholds must perform an annual review, which is essentially a less burdensome audit. Alaska requires a biennial audit, which is considered less burdensome than an annual audit requirement.

Table 7 ranks the states accounting for the various ways that audit requirements are imposed across the states

The stringency of the state’s audit mandates is a key regulatory cost that many charities must bear. The primary question for this category is whether an independent CPA audit is required.

TABLE 7

AUDIT REGULATIONS AND RANKING

| State | Audit Requirements Rankings | Revenue Threshold for Audit / Review | Independent CPA Audit Requirements |

|---|---|---|---|

| Alabama | 1 | 1 | 1 |

| Alaska | 23 | 30 | 25 |

| Arizona | 1 | 1 | 1 |

| Arkansas | 36 | 35 | 50 |

| California | 27 | 20 | 50 |

| Colorado | 1 | 1 | 1 |

| Connecticut | 36 | 35 | 50 |

| Delaware | 1 | 1 | 1 |

| Florida | 31 | 30 | 50 |

| Georgia | 31 | 30 | 50 |

| Hawaii | 50 | 50 | 50 |

| Idaho | 1 | 1 | 1 |

| Illinois | 50 | 50 | 50 |

| Indiana | 23 | 30 | 25 |

| Iowa | 1 | 1 | 1 |

| Kansas | 36 | 35 | 50 |

| Kentucky | 1 | 1 | 1 |

| Louisiana | 26 | 40 | 25 |

| Maine | 29 | 50 | 25 |

| Maryland | 36 | 35 | 50 |

| Massachusetts | 44 | 40 | 50 |

| Michigan | 44 | 40 | 50 |

| Minnesota | 31 | 30 | 50 |

| Mississippi | 49 | 45 | 50 |

| Missouri | 1 | 1 | 1 |

| Montana | 1 | 1 | 1 |

| Nebraska | 1 | 1 | 1 |

| Nevada | 1 | 1 | 1 |

| New Hampshire | 29 | 25 | 50 |

| New Jersey | 36 | 35 | 50 |

| New Mexico | 36 | 35 | 50 |

| New York | 31 | 30 | 50 |

| North Carolina | 25 | 35 | 25 |

| North Dakota | 1 | 1 | 1 |

| Ohio | 1 | 1 | 1 |

| Oklahoma | 1 | 1 | 1 |

| Oregon | 1 | 1 | 1 |

| Pennsylvania | 44 | 40 | 50 |

| Rhode Island | 36 | 35 | 50 |

| South Carolina | 1 | 1 | 1 |

| South Dakota | 1 | 1 | 1 |

| Tennessee | 36 | 35 | 50 |

| Texas | 1 | 1 | 1 |

| Utah | 1 | 1 | 1 |

| Vermont | 1 | 1 | 1 |

| Virginia | 31 | 30 | 50 |

| Washington | 27 | 20 | 50 |

| West Virginia | 44 | 40 | 50 |

| Wisconsin | 44 | 40 | 50 |

| Wyoming | 1 | 1 | 1 |

The states without the audit requirement, or requirement for audits for public contracts, are all ranked as having the least burdensome environment. Hawaii, Illinois and Mississippi impose the most burdensome audit requirements.

CATEGORY 5:

GENERAL OVERSIGHT REGULATIONS

Finally, there are several important state regulations that have not been addressed in the previous four categories. First is the issue of sales taxes. While most states exempt purchases by charities from state sales and use taxes, 19 states, to some extent, do not give charities such consideration. The states that subject charitable organizations to the state sales and use tax increase their costs of operating making it more difficult for them to fulfill their missions.

Second, states differ from one another regarding whether charitable contributions are tax deductible for residents from state income taxes, partially deductible, or not at all deductible. From a donor perspective, the lack of tax deductibility raises the net cost of giving for those donors where itemizing tax deductions is worthwhile. For example, a donor who is in a 24% federal tax bracket18 can reduce her tax liability by $240 for every $1,000 in donations. Thus, the net cost of the charitable donation is not $1,000 but $760. If available at the state level, the deductions reduce the net costs even more. Prohibiting such deductions eliminates the potential benefits, raising the net costs of their donation. These higher costs diminish the incentive and ability of donors to support charitable organizations to the extent they would otherwise desire.

Finally, there are broader regulatory considerations that can add additional compliance burdens on charitable organizations. These are whether the states require additional oversight of charitable organizations’ commercial co-ventures and whether the state used both the attorney general’s (AG) office and additional agencies to regulate charities, or whether the state is an AG-only regulated jurisdiction. Having multiple regulatory agencies increases the compliance and complexity costs on charities operating in what is referred to as a bifurcated jurisdiction.19

TABLE 8

GENERAL OVERSIGHT REGULATIONS AND RANKING

Seven states are tied for the best general oversight regulations: Alaska, Delaware, Kentucky, Montana, New Mexico, Texas and Wyoming. The six states tied for the most burdensome general oversight regulations are Connecticut, Florida, Mississippi, New Jersey, Pennsylvania and South Carolina.

| State | General Oversight Rankings | Bifurcated Jurisdiction | Not Exempt from Sales Tax | Oversees Commercial Co-ventures | Charitable Contributions Not Tax Deductible for Residents |

|---|---|---|---|---|---|

| Alabama | 45 | 1 | 50 | 50 | 25 |

| Alaska | 1 | 1 | 1 | 1 | 1 |

| Arizona | 30 | 50 | 50 | 1 | 1 |

| Arkansas | 30 | 1 | 50 | 50 | 1 |

| California | 25 | 1 | 50 | 1 | 25 |

| Colorado | 45 | 50 | 1 | 50 | 25 |

| Connecticut | 50 | 50 | 1 | 50 | 50 |

| Delaware | 1 | 1 | 1 | 1 | 1 |

| Florida | 50 | 50 | 50 | 50 | 1 |

| Georgia | 30 | 50 | 50 | 1 | 1 |

| Hawaii | 45 | 1 | 50 | 50 | 25 |

| Idaho | 17 | 1 | 50 | 1 | 1 |

| Illinois | 17 | 1 | 1 | 1 | 50 |

| Indiana | 17 | 1 | 1 | 1 | 50 |

| Iowa | 25 | 1 | 50 | 1 | 25 |

| Kansas | 30 | 50 | 50 | 1 | 1 |

| Kentucky | 1 | 1 | 1 | 1 | 1 |

| Louisiana | 30 | 1 | 50 | 50 | 1 |

| Maine | 25 | 50 | 1 | 1 | 25 |

| Maryland | 17 | 50 | 1 | 1 | 1 |

| Massachusetts | 30 | 1 | 1 | 50 | 50 |

| Michigan | 17 | 1 | 1 | 1 | 50 |

| Minnesota | 13 | 1 | 1 | 1 | 25 |

| Mississippi | 50 | 50 | 50 | 50 | 1 |

| Missouri | 13 | 1 | 1 | 1 | 25 |

| Montana | 1 | 1 | 1 | 1 | 1 |

| Nebraska | 17 | 1 | 50 | 1 | 1 |

| Nevada | 17 | 50 | 1 | 1 | 1 |

| New Hampshire | 30 | 1 | 1 | 50 | 50 |

| New Jersey | 50 | 50 | 1 | 50 | 50 |

| New Mexico | 1 | 1 | 1 | 1 | 1 |

| New York | 25 | 1 | 1 | 50 | 25 |

| North Carolina | 30 | 50 | 50 | 1 | 1 |

| North Dakota | 30 | 50 | 50 | 1 | 1 |

| Ohio | 30 | 1 | 1 | 50 | 50 |

| Oklahoma | 30 | 50 | 50 | 50 | 1 |

| Oregon | 17 | 1 | 1 | 50 | 1 |

| Pennsylvania | 50 | 50 | 1 | 50 | 50 |

| Rhode Island | 30 | 50 | 1 | 1 | 50 |

| South Carolina | 50 | 50 | 50 | 50 | 1 |

| South Dakota | 13 | 1 | 25 | 1 | 1 |

| Tennessee | 30 | 50 | 1 | 50 | 1 |

| Texas | 1 | 1 | 1 | 1 | 1 |

| Utah | 45 | 50 | 1 | 50 | 25 |

| Vermont | 13 | 1 | 1 | 1 | 25 |

| Virginia | 45 | 50 | 1 | 50 | 25 |

| Washington | 30 | 50 | 50 | 1 | 1 |

| West Virginia | 30 | 50 | 1 | 1 | 50 |

| Wisconsin | 25 | 50 | 1 | 1 | 25 |

| Wyoming | 1 | 1 | 1 | 1 | 1 |

Overall State Rankings

The overall rankings are estimated by summing together the scores for each category. The state with the lowest total score (Montana) was assigned the best rank (1), while the state with the highest total score (Pennsylvania) was assigned the worst rank (50). This methodology indicates that all five categories were given an equal weighting in the determination of the overall ranking.

TABLE 9

OVERALL STATE RANKINGS

| State | Start-Up | Annual Reporting / Filing | Paid Solicitor Fees and Regulations | Audit Requirements | Oversight Regulations | Total Rank by Category |

|---|---|---|---|---|---|---|

| Alabama | 23 | 9 | 25 | 1 | 45 | 20 |

| Alaska | 36 | 24 | 24 | 23 | 1 | 21 |

| Arizona | 7 | 12 | 1 | 1 | 30 | 8 |

| Arkansas | 26 | 7 | 35 | 36 | 30 | 29 |

| California | 33 | 50 | 43 | 27 | 25 | 42 |

| Colorado | 15 | 28 | 12 | 1 | 45 | 17 |

| Connecticut | 38 | 39 | 28 | 36 | 50 | 46 |

| Delaware | 8 | 9 | 1 | 1 | 1 | 4 |

| Florida | 44 | 46 | 46 | 31 | 50 | 49 |

| Georgia | 45 | 42 | 25 | 31 | 30 | 40 |

| Hawaii | 22 | 47 | 32 | 50 | 45 | 43 |

| Idaho | 11 | 3 | 1 | 1 | 17 | 5 |

| Illinois | 16 | 22 | 38 | 50 | 17 | 28 |

| Indiana | 1 | 12 | 50 | 23 | 17 | 18 |

| Iowa | 3 | 1 | 11 | 1 | 1 | 6 |

| Kansas | 29 | 37 | 22 | 36 | 30 | 35 |

| Kentucky | 18 | 15 | 42 | 1 | 1 | 12 |

| Louisiana | 38 | 4 | 17 | 26 | 30 | 24 |

| Maine | 34 | 33 | 19 | 29 | 25 | 32 |

| Maryland | 50 | 41 | 49 | 36 | 17 | 45 |

| Massachusetts | 43 | 35 | 43 | 44 | 30 | 44 |

| Michigan | 19 | 17 | 14 | 44 | 17 | 23 |

| Minnesota | 36 | 31 | 48 | 31 | 13 | 33 |

| Mississippi | 38 | 16 | 47 | 49 | 50 | 47 |

| Missouri | 24 | 27 | 21 | 1 | 13 | 14 |

| Montana | 3 | 8 | 1 | 1 | 1 | 1 |

| Nebraska | 2 | 2 | 1 | 1 | 17 | 3 |

| Nevada | 13 | 18 | 1 | 1 | 17 | 9 |

| New Hampshire | 27 | 35 | 39 | 29 | 30 | 36 |

| New Jersey | 47 | 38 | 28 | 36 | 50 | 48 |

| New Mexico | 10 | 18 | 9 | 36 | 1 | 16 |

| New York | 38 | 21 | 25 | 31 | 25 | 31 |

| North Carolina | 46 | 26 | 35 | 25 | 30 | 34 |

| North Dakota | 16 | 5 | 17 | 1 | 30 | 13 |

| Ohio | 48 | 39 | 32 | 1 | 30 | 26 |

| Oklahoma | 32 | 25 | 8 | 1 | 30 | 15 |

| Oregon | 12 | 49 | 35 | 1 | 17 | 19 |

| Pennsylvania | 49 | 43 | 32 | 44 | 50 | 50 |

| Rhode Island | 42 | 48 | 14 | 36 | 30 | 39 |

| South Carolina | 50 | 30 | 40 | 1 | 50 | 25 |

| South Dakota | 6 | 5 | 12 | 1 | 13 | 7 |

| Tennessee | 24 | 45 | 43 | 36 | 30 | 41 |

| Texas | 19 | 14 | 9 | 1 | 1 | 10 |

| Utah | 35 | 29 | 22 | 1 | 45 | 22 |

| Vermont | 9 | 18 | 28 | 1 | 13 | 11 |

| Virginia | 27 | 33 | 28 | 31 | 45 | 38 |

| Washington | 21 | 32 | 20 | 27 | 27 | 27 |

| West Virginia | 30 | 43 | 14 | 44 | 30 | 37 |

| Wisconsin | 14 | 23 | 41 | 44 | 25 | 29 |

| Wyoming | 5 | 9 | 1 | 1 | 1 | 2 |

An equal weighted approach was employed for the overall rankings because, while it is expected that some categories will matter more than others, it is unlikely these preferences are universal across charitable organizations. For instance, a poorly funded start-up charity would likely find burdensome startup regulations a more problematic barrier to operations than a well-funded charitable organization that has been operating for many years. Similarly, charities with no intention of employing a paid solicitor will not care about the burden imposed on these organizations, while those charities relying on these services may have a great interest in these issues.

While different weighting priorities across the five categories would alter the results, the consistently strong performance across all the categories exhibited by the top states and the consistently weak performance across all the categories exhibited by the bottom states indicate that changing the category weighting is unlikely to alter the top/bottom performers. However, it is hoped that by presenting the details by categories, readers can adjust the rankings to reflect their priorities.

Conclusion

The purpose of the rankings is to leverage the available data resources to create an ordinal quantitative ranking of each state’s approach toward regulating the charitable sector. By relating these rankings to the vibrancy of the charitable sector (as measured by the number of charities per billion dollars of GDP), it is hoped the rankings provide perspective regarding the consequences from imposing a more burdensome regulatory environment on charitable organizations.

While more research is required, this analysis shows the states imposing excessively burdensome regulatory environments may be paying a cost in terms of a less effective charitable sector. Promoting a more efficient charitable sector requires reforms, consequently, that streamline state regulations and eliminate those regulations that are unnecessary or overly burdensome.

Data Appendix A

START-UP REGULATION DATA

| State | Top Registration Fee | Requires Registration by Charitable Organizations | Incorporation Fee(s) | Charitable Organizations Exempt from Federal Income Tax Must Apply for Exemption from State Corporate Income Tax |

|---|---|---|---|---|

| Alabama | $25.00 | Yes | $100.00 | No |

| Alaska | $40.00 | Yes | $50.00 | Yes |

| Arizona | $0.00 | No | $40.00 | No |

| Arkansas | $0.00 | Yes | $50.00 | Yes |

| California | $25.00 | Yes | $50.00 | Yes |

| Colorado | $10.00 | Yes | $50.00 | No |

| Connecticut | $50.00 | Yes | $50.00 | Yes |

| Delaware | $0.00 | No | $89.00 | No |

| Florida | $400.00 | Yes | $35.00 | Yes |

| Georgia | $35.00 | Yes | $100.00 | Yes |

| Hawaii | $0.00 | Yes | $25.00 | Yes |

| Idaho | $0.00 | No | $30.00 | Yes |

| Illinois | $15.00 | Yes | $50.00 | No |

| Indiana | $0.00 | No | $0.00 | No |

| Iowa | $0.00 | No | $20.00 | No |

| Kansas | $35.00 | Yes | $20.00 | Yes |

| Kentucky | $0.00 | Yes | $8.00 | Yes |

| Louisiana | $25.00 | Yes | $75.00 | Yes |

| Maine | $50.00 | Yes | $40.00 | Yes |

| Maryland | $300.00 | Yes | $120.00 | Yes |

| Massachusetts | $100.00 | Yes | $35.00 | Yes |

| Michigan | $0.00 | Yes | $20.00 | Yes |

| Minnesota | $25.00 | Yes | $70.00 | Yes |

| Mississippi | $50.00 | Yes | $50.00 | Yes |

| Missouri | $15.00 | Yes | $25.00 | Yes |

| Montana | $0.00 | No | $20.00 | No |

| Nebraska | $0.00 | No | $10.00 | No |

| Nevada | $0.00 | Yes | $75.00 | No |

| New Hampshire | $25.00 | Yes | $25.00 | Yes |

| New Jersey | $250.00 | Yes | $75.00 | Yes |

| New Mexico | $0.00 | Yes | $25.00 | No |

| New York | $25.00 | Yes | $75.00 | Yes |

| North Carolina | $200.00 | Yes | $60.00 | Yes |

| North Dakota | $25.00 | Yes | $40.00 | No |

| Ohio | $200.00 | Yes | $125.00 | Yes |

| Oklahoma | $65.00 | Yes | $25.00 | Yes |

| Oregon | $0.00 | Yes | $50.00 | No |

| Pennsylvania | $250.00 | Yes | $125.00 | Yes |

| Rhode Island | $90.00 | Yes | $35.00 | Yes |

| South Carolina | $50.00 | Yes | $25.00 | Yes |

| South Dakota | $0.00 | No | $30.00 | No |

| Tennessee | $50.00 | Yes | $100.00 | No |

| Texas | $250.00 | Yes | $25.00 | No |

| Utah | $100.00 | Yes | $30.00 | Yes |

| Vermont | $0.00 | No | $125.00 | No |

| Virginia | $100.00 | Yes | $75.00 | No |

| Washington | $60.00 | Yes | $30.00 | No |

| West Virginia | $50.00 | Yes | $25.00 | Yes |

| Wisconsin | $15.00 | Yes | $35.00 | No |

| Wyoming | $0.00 | No | $25.00 | No |

Data Appendix B

ANNUAL REPORTING AND FILING DATA

| State | Annual Report Filing Fees | File Annual Report* | Additional Annual Filings (e.g., a Separate Annual Financial Report, Statement of Information)* | Additional Annual Filing Fees |

|---|---|---|---|---|

| Alabama | $25.00 | 1 | $0.00 | |

| Alaska | $40.00 | 1 | 1 | $25.00 |

| Arizona | $10.00 | 1 | 1 | $0.00 |

| Arkansas | $0.00 | 1 | 1 | $0.00 |

| California | $300.00 | 1 | 4 | $45.00 |

| Colorado | $0.00 | 1 | 2 | $20.00 |

| Connecticut | $50.00 | 1 | 1 | $50.00 |

| Delaware | $25.00 | 1 | $0.00 | |

| Florida | $61.25 | 1 | 1 | $400.00 |

| Georgia | $30.00 | 1 | 2 | $20.00 |

| Hawaii | $5.00 | 1 | 3 | $600.00 |

| Idaho | $0.00 | 1 | $0.00 | |

| Illinois | $10.00 | 1 | 1 | $15.00 |

| Indiana | $10.00 | 1 | 1 | $0.00 |

| Iowa | $0.00 | 1 | $0.00 | |

| Kansas | $40.00 | 1 | 1 | $35.00 |

| Kentucky | $15.00 | 1 | 1 | $0.00 |

| Louisiana | $5.00 | 1 | $0.00 | |

| Maine | $35.00 | 1 | 1 | $25.00 |

| Maryland | $200.00 | 1 | 3 | $0.00 |

| Massachusetts | $15.00 | 1 | 1 | $2,000.00 |

| Michigan | $20.00 | 1 | 1 | $0.00 |

| Minnesota | $25.00 | 1 | 1 | $35.00 |

| Mississippi | $50.00 | 1 | $0.00 | |

| Missouri | $15.00 | 1 | 1 | $15.00 |

| Montana | $15.00 | 1 | $0.00 | |

| Nebraska | $20.00 | 1 | $0.00 | |

| Nevada | $25.00 | 1 | 1 | $0.00 |

| New Hampshire | $75.00 | 1 | 1 | $5.00 |

| New Jersey | $25.00 | 1 | 1 | $250.00 |

| New Mexico | $0.00 | 1 | 1 | $10.00 |

| New York | $1,525.00 | 1 | $0.00 | |

| North Carolina | $200.00 | 1 | 1 | $0.00 |

| North Dakota | $10.00 | 1 | $0.00 | |

| Ohio | $200.00 | 1 | 0 | $25.00 |

| Oklahoma | $65.00 | 1 | 1 | $0.00 |

| Oregon | $200.00 | 1 | 2 | $50.00 |

| Pennsylvania | $0.00 | 1 | 3 | $257.00 |

| Rhode Island | $20.00 | 1 | 3 | $140.00 |

| South Carolina | $50.00 | 1 | 2 | $0.00 |

| South Dakota | $10.00 | 1 | $0.00 | |

| Tennessee | $20.00 | 1 | 2 | $240.00 |

| Texas | $0.00 | 2 | $255.00 | |

| Utah | $10.00 | 1 | 1 | $100.00 |

| Vermont | $0.00 | 1 | 1 | $10.00 |

| Virginia | $325.00 | 1 | 2 | $0.00 |

| Washington | $10.00 | 1 | 2 | $40.00 |

| West Virginia | $25.00 | 1 | 2 | $50.00 |

| Wisconsin | $54.00 | 1 | 1 | $0.00 |

| Wyoming | $25.00 | 1 | $0.00 |

Data Appendix C

PAID SOLICITOR FEES AND REGULATION DATA

| State | Solicitor Renewal Fees | Paid Solicitor Registration Fee | Requires Registration by Commercial Fundraisers | Surety Bond Requirements | Requires Notice Before Solicitation Campaign | Requires Registration by Fundraising Counsel | Requires Annual Financial Reporting by Commercial Fundraisers | Requires Filing of Contracts between Charities and Commercial Fundraisers |

|---|---|---|---|---|---|---|---|---|

| Alabama | $0.00 | $0.00 | Yes | $10,000 | No | Yes | Yes | Yes |

| Alaska | $0.00 | $200.00 | Yes | $10,000 | No | No | Yes | Yes |

| Arizona | $0.00 | $0.00 | No | $0 | No | No | No | No |

| Arkansas | $0.00 | $0.00 | Yes | $0 | Yes | Yes | Yes | Yes |

| California | $0.00 | $0.00 | Yes | $25,000 | Yes | Yes | Yes | Yes |

| Colorado | $0.00 | $0.00 | Yes | $0 | Yes | No | Yes | No |

| Connecticut | $0.00 | $0.00 | Yes | $20,000 | Yes | No | Yes | Yes |

| Delaware | $0.00 | $0.00 | No | $0 | No | No | No | No |

| Florida | $0.00 | $0.00 | Yes | $50,000 | Yes | Yes | Yes | Yes |

| Georgia | $0.00 | $0.00 | Yes | $10,000 | Yes | No | Yes | Yes |

| Hawaii | $0.00 | $0.00 | Yes | $25,000 | No | Yes | Yes | Yes |

| Idaho | $0.00 | $0.00 | No | $0 | No | No | No | No |

| Illinois | $0.00 | $100.00 | Yes | $10,000 | No | Yes | Yes | Yes |

| Indiana | $50.00 | $1,000.00 | Yes | $0 | Yes | Yes | Yes | Yes |

| Iowa | $0.00 | $10.00 | Yes | $0 | No | No | No | Yes |

| Kansas | $0.00 | $0.00 | Yes | $0 | No | Yes | Yes | Yes |

| Kentucky | $0.00 | $300.00 | Yes | $25,000 | No | Yes | Yes | Yes |

| Louisiana | $0.00 | $150.00 | Yes | $25,000 | No | No | No | Yes |

| Maine | $0.00 | $250.00 | Yes | $25,000 | No | No | Yes | No |

| Maryland | $0.00 | $350.00 | Yes | $25,000 | Yes | Yes | Yes | Yes |

| Massachusetts | $0.00 | $1,000.00 | Yes | $25,000 | No | Yes | Yes | Yes |

| Michigan | $0.00 | $0.00 | Yes | $10,000 | No | No | Yes | Yes |

| Minnesota | $0.00 | $200.00 | Yes | $20,000 | Yes | Yes | Yes | Yes |

| Mississippi | $0.00 | $250.00 | Yes | $10,000 | Yes | Yes | Yes | Yes |

| Missouri | $50.00 | $50.00 | Yes | $0 | No | No | Yes | No |

| Montana | $0.00 | $0.00 | No | $0 | No | No | No | No |

| Nebraska | $0.00 | $0.00 | No | $0 | No | No | No | No |

| Nevada | $0.00 | $0.00 | No | $0 | No | No | No | No |

| New Hampshire | $0.00 | $150.00 | Yes | $20,000 | Yes | Yes | No | Yes |

| New Jersey | $0.00 | $0.00 | Yes | $20,000 | No | Yes | Yes | Yes |

| New Mexico | $0.00 | $0.00 | Yes | $25,000 | No | No | No | Yes |

| New York | $0.00 | $0.00 | Yes | $10,000 | No | Yes | Yes | Yes |

| North Carolina | $0.00 | $0.00 | Yes | $50,000 | No | Yes | Yes | Yes |

| North Dakota | $0.00 | $0.00 | Yes | $20,000 | No | Yes | No | Yes |

| Ohio | $0.00 | $0.00 | Yes | $25,000 | Yes | No | Yes | Yes |

| Oklahoma | $0.00 | $0.00 | Yes | $0 | No | No | No | No |

| Oregon | $0.00 | $0.00 | Yes | $0 | Yes | Yes | Yes | Yes |

| Pennsylvania | $0.00 | $0.00 | Yes | $25,000 | No | Yes | Yes | Yes |

| Rhode Island | $0.00 | $0.00 | Yes | $10,000 | No | Yes | No | Yes |

| South Carolina | $0.00 | $0.00 | Yes | $15,000 | Yes | Yes | Yes | Yes |

| South Dakota | $0.00 | $0.00 | Yes | $0 | Yes | No | Yes | No |

| Tennessee | $0.00 | $0.00 | Yes | $25,000 | Yes | Yes | Yes | Yes |

| Texas | $0.00 | $0.00 | No | $25,000 | No | No | Yes | Yes |

| Utah | $0.00 | $0.00 | Yes | $0 | Yes | Yes | No | Yes |

| Vermont | $0.00 | $0.00 | Yes | $20,000 | Yes | No | Yes | Yes |

| Virginia | $0.00 | $0.00 | Yes | $20,000 | No | Yes | Yes | Yes |

| Washington | $0.00 | $0.00 | Yes | $25,000 | No | No | Yes | Yes |

| West Virginia | $0.00 | $0.00 | Yes | $10,000 | No | Yes | No | Yes |

| Wisconsin | $0.00 | $0.00 | Yes | $20,000 | Yes | Yes | Yes | Yes |

| Wyoming | $0.00 | $0.00 | No | $0 | No | No | No | No |

Data Appendix D

AUDIT REQUIREMENT DATA

| State | Require Independent CPA Audit | Require Independent CPA Audit for Public Contracts Only | Revenue Threshold for Audit | Revenue Threshold for Review |

|---|---|---|---|---|

| Alabama | No | No | ||

| Alaska | Yes* | No | $750,000 | |

| Arizona | No | No | ||

| Arkansas | Yes | No | $500,000 | |

| California | Yes | No | $2,000,000 | |

| Colorado | No | No | ||

| Connecticut | Yes | No | $500,000 | |

| Delaware | No | No | ||

| Florida | Yes | No | $1,000,000 | $500,000 |

| Georgia | Yes | No | $1,000,000 | $500,000 |

| Hawaii | Yes | No | ||

| Idaho | No | No | ||

| Illinois | Yes | No | $300,000 | $25,000 |

| Indiana | No | Yes | $750,000 | |

| Iowa | No | No | ||

| Kansas | Yes | No | $500,000 | |

| Kentucky | No | No | ||

| Louisiana | No | Yes | $500,000 | $200,000 |

| Maine | Yes* | No | ||

| Maryland | Yes | No | $750,000 | $300,000 |

| Massachusetts | Yes | No | $500,000 | $200,000 |

| Michigan | Yes | No | $500,000 | $250,000 |

| Minnesota | Yes | No | $750,000 | |

| Mississippi | Yes | No | $250,000 | |

| Missouri | No | No | ||

| Montana | No | No | ||

| Nebraska | No | No | ||

| Nevada | No | No | ||

| New Hampshire | Yes | No | $2,000,000 | $500,000 |

| New Jersey | Yes | No | $1,000,000 | $25,000 |

| New Mexico | Yes | No | $500,000 | |

| New York | Yes | No | $1,000,000 | $250,000 |

| North Carolina | No | Yes | $500,000 | |

| North Dakota | No | No | ||

| Ohio | No | No | ||

| Oklahoma | No | No | ||

| Oregon | No | No | ||

| Pennsylvania | Yes | No | $750,000 | $100,000 |

| Rhode Island | Yes | No | $500,000 | |

| South Carolina | No | No | ||

| South Dakota | No | No | ||

| Tennessee | Yes | No | $500,000 | |

| Texas | No | No | ||

| Utah | No | No | ||

| Vermont | No | No | ||

| Virginia | Yes | No | $1,000,000 | $750,000 |

| Washington | Yes | No | $3,000,000 | $1,000,000 |

| West Virginia | Yes | No | $500,000 | $300,000 |

| Wisconsin | Yes | No | $500,000 | $300,000 |

| Wyoming | No | No |

Data Appendix E

GENERAL OVERSIGHT DATA

| State | Bifurcated Jurisdiction (1 Bifurcated, 0 AG-only regulator) | Not Exempt from State Sales and Use Taxes | Oversees Commercial Co-Ventures | Charitable Contributions Tax Deductible for Residents |

|---|---|---|---|---|

| Alabama | No | Not Exempt | Yes | Limited |

| Alaska | No | Exempt | No | Full |

| Arizona | Yes | Not Exempt | No | Full |

| Arkansas | No | Not Exempt | Yes | Full |

| California | No | Not Exempt | No | Limited |

| Colorado | Yes | Exempt | Yes | Limited |

| Connecticut | Yes | Exempt | Yes | Not Allowed |

| Delaware | No | Exempt | No | Full |

| Florida | Yes | Not Exempt | Yes | Full |

| Georgia | Yes | Not Exempt | No | Full |

| Hawaii | No | Not Exempt | Yes | Limited |

| Idaho | No | Not Exempt | No | Full |

| Illinois | No | Exempt | No | Not Allowed |

| Indiana | No | Exempt | No | Not Allowed |

| Iowa | No | Not Exempt | No | Limited |

| Kansas | Yes | Not Exempt | No | Full |

| Kentucky | No | Exempt | No | Full |

| Louisiana | No | Not Exempt | Yes | Full |

| Maine | Yes | Exempt | No | Limited |

| Maryland | Yes | Exempt | No | Full |

| Massachusetts | No | Exempt | Yes | Not Allowed |

| Michigan | No | Exempt | No | Not Allowed |

| Minnesota | No | Exempt | No | Limited |

| Mississippi | Yes | Not Exempt | Yes | Full |

| Missouri | No | Exempt | No | Limited |

| Montana | No | Exempt | No | Full |

| Nebraska | No | Not Exempt | No | Full |

| Nevada | Yes | Exempt | No | Full |

| New Hampshire | No | Exempt | Yes | Not Allowed |

| New Jersey | Yes | Exempt | Yes | Not Allowed |

| New Mexico | No | Exempt | No | Full |

| New York | No | Exempt | Yes | Limited |

| North Carolina | Yes | Not Exempt | No | Full |

| North Dakota | Yes | Not Exempt | No | Full |

| Ohio | No | Exempt | Yes | Not Allowed |

| Oklahoma | Yes | Not Exempt | No | Full |

| Oregon | No | Exempt | Yes | Full |

| Pennsylvania | Yes | Exempt | Yes | Not Allowed |

| Rhode Island | Yes | Exempt | No | Not Allowed |

| South Carolina | Yes | Not Exempt | Yes | Full |

| South Dakota | No | Not Exempt | No | Full |

| Tennessee | Yes | Exempt | Yes | Full |

| Texas | No | Exempt | No | Full |

| Utah | Yes | Exempt | Yes | Limited |

| Vermont | No | Exempt | No | Limited |

| Virginia | Yes | Exempt | Yes | Limited |

| Washington | Yes | Not Exempt | No | Full |

| West Virginia | Yes | Exempt | No | Not Allowed |

| Wisconsin | Yes | Exempt | No | Limited |

| Wyoming | No | Exempt | No | Full |

Footnotes

- For further discussion on the impact of regulations on the charitable sector, see, McGuigan E “Government Overreach Hurts Charities and Those They Serve” Philanthropy Roundtable, March 19, 2022. https://www.philanthropyroundtable.org/resource/government-overreach-hurts-charities-and-those-they-serve/. ↩︎

- It is important to note that the ordinality of the rankings are the material conclusion rather than the value differences in the underlying scores. ↩︎

- Coffey, Bentley, Patrick A. McLaughlin, and Pietro Peretto. “The Cumulative Cost of Regulations.” Review of Economic Dynamics 38 (2020): 1-21. ↩︎

- Chambers D and O’Reilly C “The Regressive Effect of Regulations in California” Mercatus Center, March 2, 2021. ↩︎

- Winegarden W “The 50-State Small Business Regulation Index” Pacific Research Institute, July 2015. ↩︎

- The analysis does not apply to churches or other nonprofits that are exempt from registration requirements. Additional research that specifically addresses these organizations is an important future topic. ↩︎

- For a more detailed discussion on how the government regulatory burden acts as a tax on charitable organizations see the websites, http://www.muridae.com/nporegulation/documents/regulation_costs.html and http://www.muridae.com/nporegulation/burden.html. ↩︎

- A 2016 study by the Urban Institute provides a good overview of the types of regulations imposed, see Lott CM, Boris ET, Goldman KK, Johns BJ, Gaddy M and Farrell M “State Regulation and Enforcement in the Charitable Sector” Urban Institute, September 2016. ↩︎

- It is important to note that the ordinality of the rankings are the material conclusion rather than the value differences in the underlying scores. ↩︎

- The data are from the Internal Revenue Service (IRS) “Tax Exempt Organization Search Bulk Data Downloads”, https://www.irs.gov/charities-non-profits/tax-exempt-organization-search-bulk-data-downloads. ↩︎

- Rooney P and Bergdoll J “What happens to charitable giving when the economy falters?” The Conversation, March 23, 2020, https://theconversation.com/what-happens-to-charitable-giving-when-the-economy-falters-133903. ↩︎

- The correlation coefficient between the state rankings and the number of charitable organizations per billion dollars of GDP is -0.25. ↩︎

- These resources included: Lott CM, Shelly ML, Dietz N, and Gaddy M “Bifurcation of State Regulations of Charities” Urban Institute, March 2018; and “Nonprofit Registration & Compliance” Hurwit & Associates, https://www.hurwitassociates.com/nonprofit-registration-and-compliance/ (accessed October 2022, multiple times); “Demystifying the Need for Nonprofits to Register in All 50 States in Order to Fundraise Nationally” AMC Consulting, July 9, 2021, https://www.alexcounts.com/blog/2021/7/9/demystifying-the-need-for-nonprofits-to-register-in-all-50-states-in-order-to-fundraise-nationally; “Summary Survey of State Charity Registration Requirements in All 50 States and the District of Columbia” Lowenstein Sandler LLP, December 2019. ↩︎

- Lott CM, Shelly ML, Dietz N, and Gaddy M “Bifurcation of State Regulations of Charities” Urban Institute, March 2018; and “Nonprofit Registration & Compliance” Hurwit & Associates, https://www.hurwitassociates.com/nonprofit-registration-andcompliance/ (accessed October 2022, multiple times); and National Council of Nonprofits, https://www.councilofnonprofits.org/nonprofit-audit-guide/state-law-audit-requirements. ↩︎

- See: Lott CM, Shelly ML, Dietz N, and Gaddy M “Bifurcation of State Regulations of Charities” Urban Institute, March 2018; and “Demystifying the Need for Nonprofits to Register in All 50 States in Order to Fundraise Nationally” AMC Consulting, July 9, 2021, https://www.alexcounts.com/blog/2021/7/9/demystifying-the-need-for-nonprofits-to-register-in-all-50-states-inorder-to-fundraise-nationally. ↩︎

- See: “Summary Survey of State Charity Registration Requirements in All 50 States and the District of Columbia” Lowenstein Sandler LLP, December 2019. ↩︎

- Audit requirement data is based on the database maintained by: National Council of Nonprofits, https://www.councilofnonprofits.org/nonprofit-audit-guide/state-law-audit-requirements (accessed September 3, 2022). ↩︎

- Foster S, “2021-2022 tax brackets and federal income tax rates” Bankrate.com, https://www.bankrate.com/taxes/taxbrackets/ (accessed September 3, 2022). ↩︎

- See: Lott CM, Shelly ML, Dietz N, and Gaddy M “Bifurcation of State Regulations of Charities” Urban Institute, March 2018. ↩︎